Award-winning PDF software

form 3949-a - how to report tax fraud - formswift

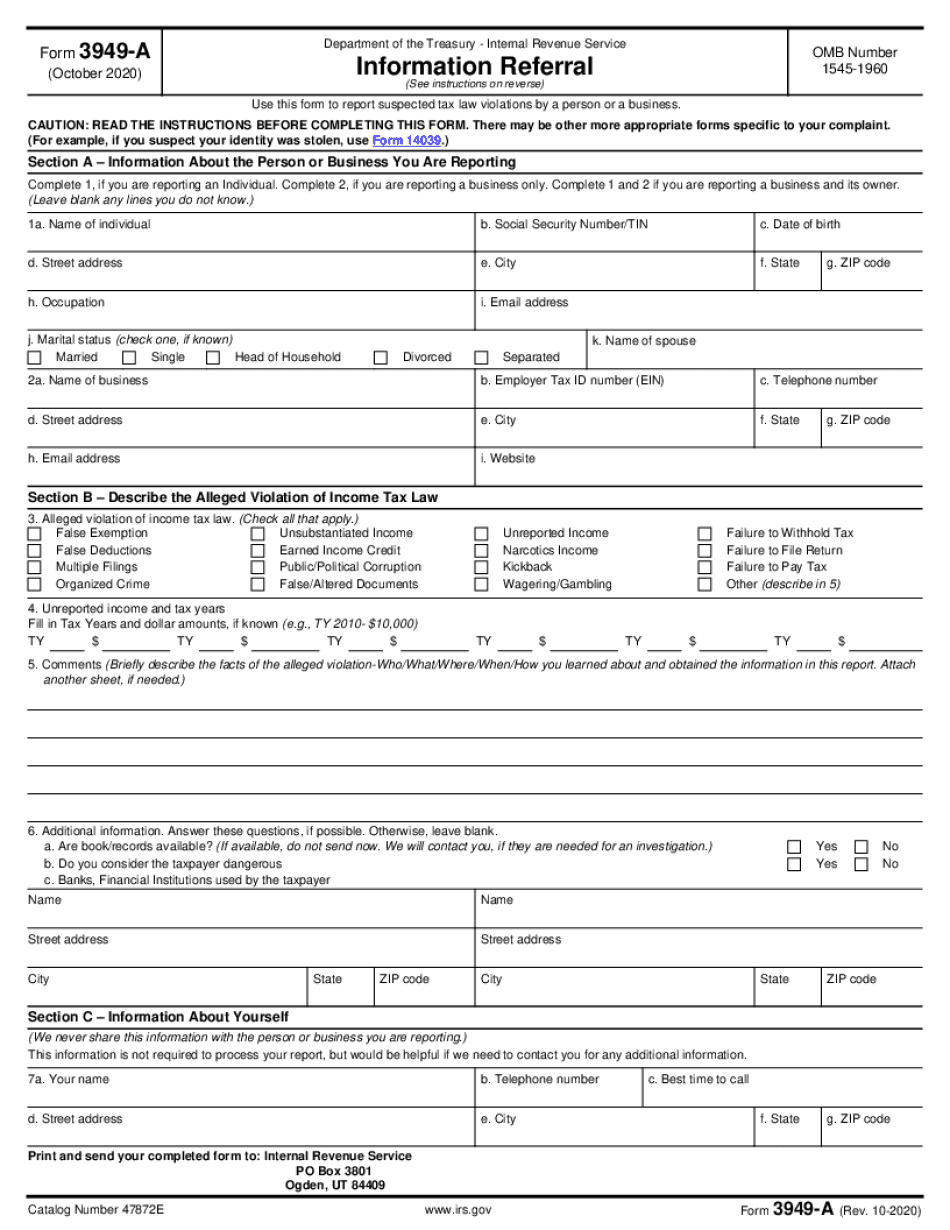

Is used to inform the IRS that a person who believes that he or she will be adversely affected by the tax consequences of filing a Form 3949-A has provided his or her written request to the IRS for a Form 3949-A. (2). . . Once an IRS Form 3949-A is received, the IRS will contact the person to seek his or her comments on the contents of the filing. The review of the Form 3949-A does not mean that the taxpayer will be liable for the tax consequences of (3). . . (4). . . (5). . . The IRS shall prepare and return to the person a written response to the request. If no written response is received, the taxpayer may request a hearing before a commissioner. If a taxpayer cannot resolve the case before an administrative hearing, the Treasury Inspector General for Tax Administration (TI GTA) may.

Instructions for form d-3949a, tax fraud and identity theft

State, ?. State, ?. If state, you can leave it blank. If state, you can leave it blank. Include the type and amount of tax withheld (see next section for form D-3952), if applicable. If you are self-employed, you must enter the total tax withheld from the employee's paycheck. It does not apply if the taxpayer's tax return has been accepted or is being filed electronically. For more detailed information on Form D-3951 (for taxpayers who choose to report a return online, not paid to a bank) and D-3952 (for taxpayers who choose to report to a bank), click here. D-4038 (Self-Employed) Self-employed individuals or the sole proprietors of small business entities (SERB), are required to file Form D-4038. You can choose to file by paper or online (if you use Form D-4040 or D-4041). If filing by paper, prepare the completed form at home and hand it to your taxpayer representative at the IRS. The.

Fillable form 3949-a | edit, sign & download in pdf | pdfrun

The Internal Revenue Code of 1986. (Section 6041-B of the Internal Revenue Code) The Internal Revenue Code of 1986, as amended, is the federal tax code for the United States. The Taxpayer (or taxpayers) must comply with federal tax regulations. The IRS considers the following taxpayers to be tax delinquent: (a) A taxpayer who owes more than 25,000, but does not owe tax due under federal statute: (1) who willfully fails to file a timely return, or (2) whose return or return and supporting documents are inaccurate or fraudulently obtained. (b) A taxpayer who owes the maximum tax under federal statutes, or who is subject to audit. Any taxpayer who is subject to United States tax reporting requirements under tax laws, but fails to file a timely return or to furnish any information required under those laws or under federal statutes (including. . . The IRC (6013) also imposes a tax.

Can someone “turn me in” to the ?

I have been in the IRS for more than 25 years,” says Robert Opp Jr., a former chief of staff to acting IRS Commissioner Daniel Were. “We never did anything wrong. And the way the [intelligence] programs came out and were described was that this is all about stopping tax fraud, but there has never been any evidence or any reason to believe the people we put at risk in the field were engaged in tax fraud. If you want to get a sense of how badly these groups have been treated by the IRS, look at the [form 3949-A] program.” (The form is often referred to as “the Stingray.”) In 2010, the form became one of the first “intelligence-sharing” programs for intelligence agencies, following the passage of the USA PATRIOT Act. “What the program really was is a new tool for gathering information about.

Get and sign form 3949 a -signnow

Information is available only to Covered Entities. Covered Entities may direct that the Form be provided to the IRS via Form 3949-A. The information referred to in the request may include: Information about the Covered Entity, including business titles or place of organization (if the name does not appear on a Form 990-EZ, the Covered Entity must indicate the name that appears on a current letterhead or similar business document issued pursuant to the tax laws) and business location (if the information appears on a Form 990-EZ) Covered Entities may directly request the information from the person that issued the Form 990-EZ and must provide their reasons for requesting the information Covered Entities have the option of submitting the Information referred to in the requested information with the Request for Information and Certification (RFI) or through direct request through the IRS. Request for Information and Certification (RFI) (IRS EO 13673-E) may be processed through Internal Revenue.